The Role of LOIs in M&As: Structuring Letters of Intent

-1.png?width=760&height=428&name=Copy%20of%20Blog%20Header%20Images%20(2)-1.png)

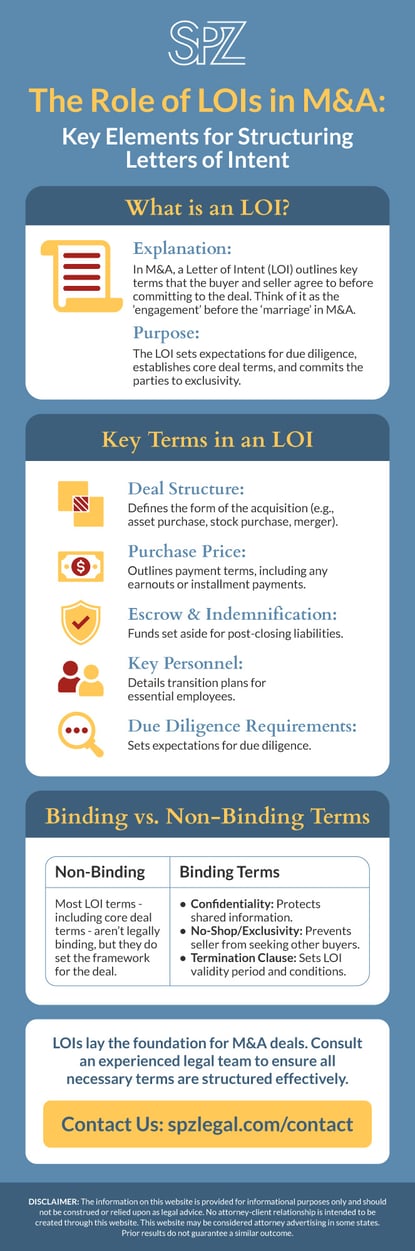

Letters of Intent (LOIs) play a crucial role in M&A transactions, setting a preliminary framework for the buyer and seller to agree on essential terms before fully committing to the deal. Here, we break down what an LOI is, when it's used, and its binding terms to help founders understand its significance and structure it effectively.

What is an LOI in M&A?

In mergers and acquisitions (M&A), an LOI is like a "term sheet," outlining the key business, legal, and tax terms that both parties agree on to initiate the deal. Typically presented by the buyer, the LOI signals the buyer and seller’s intent to invest significant resources into due diligence and other M&A steps. Think of it as the “engagement” before the “marriage” in an M&A transaction, aligning both parties on fundamental terms.

When is an LOI Typically Signed?

LOIs usually come after preliminary business and financial diligence and before a deep dive into the seller's legal and contractual landscape. This stage allows both parties to agree on key deal terms while leaving room for adjustments based on further findings.

![]()

Are LOIs Legally Binding?

Generally, LOIs are not legally binding, meaning the parties are not yet obligated to close the deal. However, LOIs do often include specific binding terms, such as:

Generally, LOIs are not legally binding, meaning the parties are not yet obligated to close the deal. However, LOIs do often include specific binding terms, such as:

- Confidentiality: Ensures all information gathered during the process is protected.

- No-Shop/Exclusivity: The seller agrees not to pursue other potential buyers for a set period.

- Termination Clause: Specifies how long the LOI is valid and the conditions for termination.

Although LOIs are generally non-binding, backing out without cause can damage reputations and, in rare cases, lead to legal consequences if certain binding clauses are breached.

Key Terms in an LOI

An LOI typically includes several critical terms to streamline negotiations and minimize risks:

- Deal Structure: Defines the form of the acquisition (e.g., asset purchase, stock purchase, merger).

- Purchase Price and Mechanics: Outlines payment terms, which may include an initial closing payment, earnouts based on post-closing performance, installment payments, and/or some combination.

- Escrow and Indemnification: Describes funds that may be held to cover any post-closing liabilities, and sometimes LOIs will specify high-level terms around indemnification duration and caps.

- Key Personnel Treatment: Determines how key employees will be managed in the transition.

- Due Diligence Requirements: Sets expectations for additional investigation before closing.

![]()

Although Letters of Intent do not typically set the terms of the deal in stone, the terms in an LOI are hard to renegotiate after the fact. As such, LOIs are foundational in structuring M&A deals, providing a blueprint for negotiations and protecting both parties. Engaging with an experienced legal team, like SPZ Legal, during this stage can help founders ensure that all necessary terms are negotiated effectively, reducing risks and positioning the deal for a smoother closing.

For more on structuring M&A deals or to discuss your specific needs, reach out to our team at SPZ Legal for experienced guidance.

![]()

Categories

Recent Posts

- Converting an LLC to a Corporation: When It Makes Sense and How to Do It Without Creating a Mess

- Exit Structures: Mergers, Acquisitions, & Tax Treatment

- Due Diligence Best Practices: Be Prepared for M&A Success

- SPZ Legal Advises Mosey in Its Acquisition by Gusto

- Why AI-First Founders Choose AI-Savvy Startup Lawyers

- Promotions to Senior Startup Counsel: Recognizing Experience, Investing in Careers

- SPZ Legal Earns Back-to-Back Recognition in Chambers Spotlight California 2026